When the first generic version of a popular brand-name drug hits the market, it doesn’t mean the battle is over-it’s just beginning. The real story of generic drug competition isn’t about one company beating the patent. It’s about what happens after that first entry. And that’s where things get messy, fast.

How the First Generic Gets a Head Start

Under the Hatch-Waxman Act of 1984, the first generic company to challenge a brand-name drug’s patent and win gets a special prize: 180 days of exclusive rights to sell their version. During this time, they face no direct competition. This isn’t just a reward-it’s a financial lifeline. Developing a generic drug and fighting a patent lawsuit can cost $5 million to $10 million. The 180-day exclusivity period lets that first entrant charge 70-90% of the brand’s price and capture 70-80% of the market. That’s how they pay back their investment.Take Crestor, for example. When the first generic arrived in 2016, the brand was selling for $320 a month. The first generic hit the market at $120. Within 18 months, with eight competitors on the shelf, the price dropped to $10. That’s not a coincidence. It’s the result of a predictable pattern: one winner, then a flood.

The Second Entrant Changes Everything

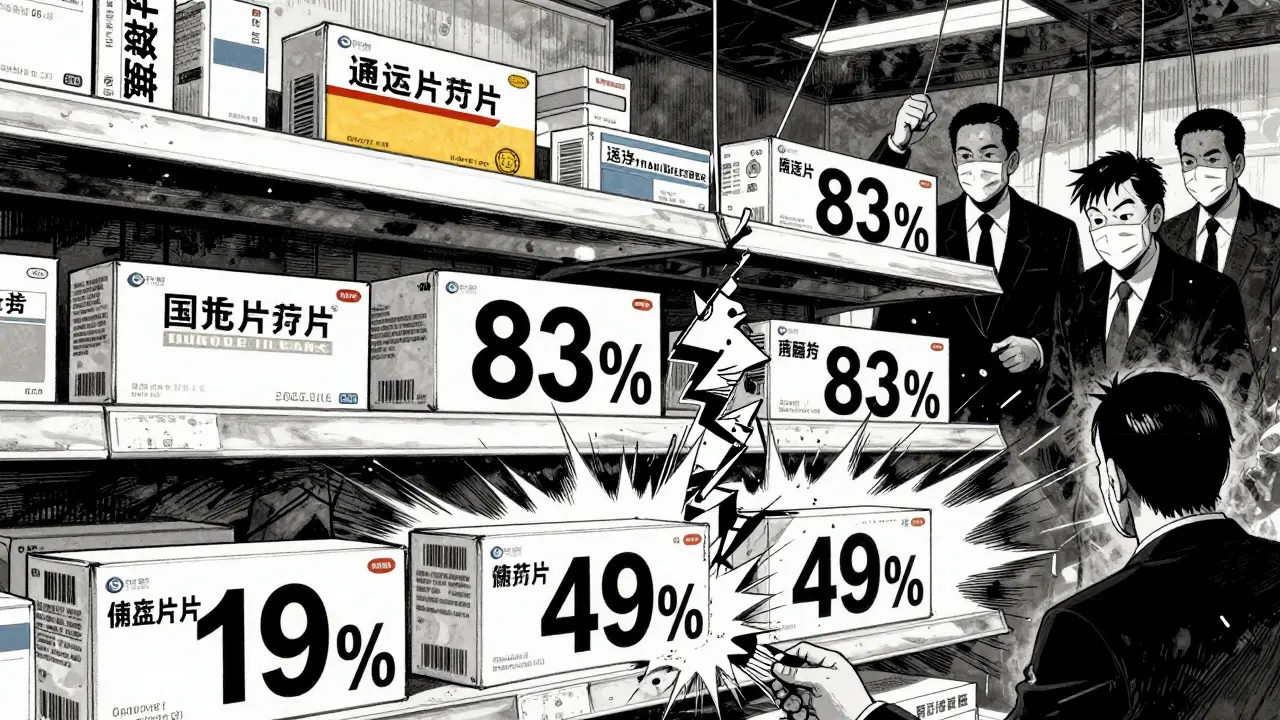

The moment that 180-day clock runs out, other companies jump in. And here’s the kicker: the biggest price drop doesn’t happen between the brand and the first generic. It happens between the second and third generics.According to the FDA’s 2022 report, when there’s one generic, prices are at 83% of the brand. Add a second, and they drop to 66%. Add a third? They crash to 49%. That’s a 25-30% plunge in just one step. Why? Because the market shifts from scarcity to surplus. Pharmacies and insurers start playing companies against each other. The second entrant doesn’t just compete on price-they compete on speed, reliability, and who can get into the formulary first.

But here’s the twist: the second entrant doesn’t always win. Sometimes, the brand company launches its own version-a so-called “authorized generic.” Merck did this with Januvia in 2019. On the exact day the first generic entered, Merck’s subsidiary started selling the same drug under a different label. Within six months, they grabbed 32% of the market. That meant the first generic’s share dropped from 80% to under 50%. The authorized generic isn’t a loophole-it’s a legal strategy. And 65% of brand companies use it when they see a big market coming.

Why Later Entrants Struggle Even When They’re Approved

You’d think that once the FDA approves a generic, it’s a free-for-all. But that’s not how the U.S. system works. Getting approval is only half the battle. The real hurdle is getting into pharmacies and insurance plans.Pharmacy Benefit Managers (PBMs)-the middlemen between insurers and pharmacies-control access. And they don’t care who got approved first. They care about who offers the lowest price. In 2023, 68% of PBM contracts used a “winner-take-all” model. That means if you’re the cheapest, you get 80-90% of the business. The others? They get scraps.

And getting to that price point takes time. While the first generic might get formulary placement in 3-6 months, subsequent entrants often wait 9-12 months. During that time, they’re approved but invisible. Patients can’t get their prescriptions filled. Manufacturers lose money. Some just quit.

The Hidden Cost: Manufacturing and Shortages

Generic drugs are made in factories-often the same ones. And here’s the problem: as more companies enter, they all start relying on the same contract manufacturers. By 2022, 78% of second- and later-stage generic manufacturers used contract facilities, compared to just 45% of the first entrant. Why? Because building your own plant costs tens of millions. It’s cheaper to rent space.But when one factory has a quality issue-say, a contaminated batch or a failed inspection-it doesn’t just affect one drug. It affects dozens. The FDA found that 62% of generic drug shortages in 2022 happened in products with three or more manufacturers. That’s not bad luck. It’s systemic risk. One plant failure can trigger nationwide shortages of blood pressure pills, diabetes meds, or antibiotics.

And it’s getting worse. Between 2018 and 2022, the number of companies making generics dropped from 142 to 97. The market is consolidating. The companies that survive aren’t the ones with the cheapest pills. They’re the ones with the most reliable supply chains, the strongest PBM deals, and the ability to handle complex drugs.

Complex Generics Are the New Gold Mine

Not all generics are created equal. Simple pills-like metformin or lisinopril-are now battlegrounds with 5-10 competitors. Prices are at 10-15% of the brand. Profit margins are razor-thin. But complex generics? Those are different.Think inhalers, injectables, or topical creams that require special delivery systems. These take longer to develop. Fewer companies can make them. And the FDA requires extra testing. That means fewer competitors. In these markets, you might only see 2-3 players. Prices hover around 30-40% of the brand. That’s still a big drop from the original, but it’s enough to make money.

Companies are shifting strategy. Some are becoming “innovation players,” focusing on these harder-to-make drugs. Others are “efficiency players,” trying to outlast the competition on cost. The winners? The ones who can navigate both the regulatory maze and the PBM negotiation game.

What’s Next? Staggered Entry and Legal Games

The patent fight isn’t over when the first generic wins. Sometimes, brand companies and generic manufacturers strike deals. In 2022, there were 147 patent settlement agreements-and 65% of them included staggered entry dates. That means instead of a free-for-all, competitors enter one after another, over months or even years.Take Humira. Six biosimilar companies agreed to enter the market between 2023 and 2025. That’s not because they’re being nice. It’s because they want to avoid a price war that could collapse the whole market. These deals are legal, but they’re controversial. Critics say they delay competition. Supporters say they prevent chaos.

Meanwhile, brand companies are filing more citizen petitions-1,247 between 2018 and 2022. Each one delays a generic by an average of 8.3 months. These aren’t health concerns. They’re legal tactics. And they’re working. One petition can kill a company’s entire entry plan.

The Bigger Picture: Why Prices Keep Falling

The U.S. doesn’t have price controls. So why do generic prices keep dropping? Because competition works differently here. In Germany or Japan, prices stabilize after a few competitors enter. In the U.S., they keep falling-sometimes to 10% of the brand price. Why? PBMs. Retailers. Hospitals. All of them are negotiating aggressively.And it’s not sustainable. When prices fall too fast, manufacturers can’t make money. They shut down production. Shortages follow. Then the cycle repeats. Experts like Dr. Aaron Kesselheim warn this system creates perverse incentives: too many companies chase the same low-margin drugs, and none can survive long-term.

Some propose solutions: long-term contracts, restricted entry for simple generics, or even price floors. But none have stuck. For now, the market runs on speed, cost, and timing. And the companies that win aren’t the ones with the best science. They’re the ones who understand the game.

What is the 180-day exclusivity period for generic drugs?

The 180-day exclusivity period is a legal incentive given to the first generic drug manufacturer that successfully challenges a brand-name drug’s patent under the Hatch-Waxman Act. During this time, no other generic can enter the market, allowing the first entrant to capture 70-80% of sales at prices 70-90% of the brand. This period helps them recover litigation and development costs, which can reach $5-10 million.

Why do generic drug prices drop so sharply after the second entrant?

The biggest price drops happen between the second and third generic competitors because the market shifts from limited supply to oversupply. With one generic, prices are at 83% of the brand. With two, they fall to 66%. With three, they crash to 49%. This happens because pharmacies and insurers start using competitive bidding to drive prices down. Each new entrant undercuts the last, and the pressure builds fast.

Can brand companies compete with their own generics?

Yes. Brand companies often launch “authorized generics”-versions of their own drug sold under a different label, usually through a subsidiary. These are identical to the generic in active ingredients and quality. Merck did this with Januvia in 2019, capturing 32% of the market within six months and cutting the first generic’s share in half. About 65% of brand companies use this tactic when they expect heavy generic competition.

Why are there so many generic drug shortages?

Shortages often occur when three or more manufacturers make the same drug using the same contract manufacturing facilities. If one factory has a quality issue-like contamination or failed inspections-it can halt supply for multiple brands. In 2022, 62% of generic shortages involved products with three or more makers. The pressure to cut costs leads companies to rely on shared suppliers, creating systemic vulnerability.

How do Pharmacy Benefit Managers (PBMs) affect generic competition?

PBMs control which generics get covered by insurance plans. In 2023, 68% of PBM contracts used a “winner-take-all” model, where the lowest bidder gets 80-90% of the business. This means even if a company gets FDA approval first, they might not get access to patients if they don’t offer the lowest price. PBMs have turned generic competition into a race to the bottom, often leaving manufacturers with unsustainable margins.

What’s the difference between simple and complex generics?

Simple generics are pills like metformin or atorvastatin-easy to manufacture and replicate. These markets attract 5-10+ competitors and prices drop to 10-15% of the brand. Complex generics-like inhalers, injectables, or topical creams-require advanced technology and more testing. Fewer companies can make them, so competition is limited to 2-3 players, and prices stay higher at 30-40% of the brand. These are now the most profitable segment for generic manufacturers.

Final Thoughts: The Game Has Changed

The generic drug market used to be about beating the patent. Now it’s about beating the system. The first entrant wins the race. But the real winners are the ones who understand the next moves: how to time entry, how to navigate PBMs, how to avoid supply chain traps, and when to walk away from a race that’s already been run.Companies that treat generics like a commodity are disappearing. The survivors are building strategy, not just pills.

MALYN RICABLANCA

March 17, 2026 at 19:03

This whole system is a circus!! 🎪 The first generic gets 180 days of monopoly money, then BAM-everyone else charges in like it’s Black Friday at Walmart. And don’t even get me started on authorized generics-brand companies playing both sides like shady poker players! It’s not competition, it’s psychological warfare with pill bottles. The FDA? They’re just watching from the sidelines like it’s a reality show. Who’s winning? The PBMs. Who’s losing? Patients. And the manufacturers? They’re just ghosts in the machine. 😭